Deep Learning for Event-Driven Stock Prediction (Paper Summary)

18 Aug 2017Here is the link to the paper.

Summary

The aim is to be able to predict the price movement using long-term and short-term events, as reported in the news. It is framed as a classification problem. The approach is to first learn event embeddings from the news events. Embeddings for long-term and short-term events are then considered together in a feed-forward network to predict the final class.

Dataset

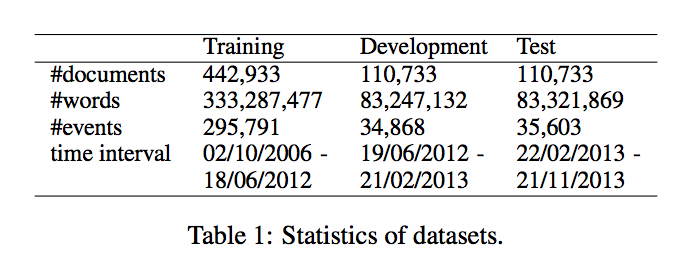

They gathered about 10 million news events from Reuters and Bloomberg with timestamps ranging from Oct 2006 to Nov 2013.

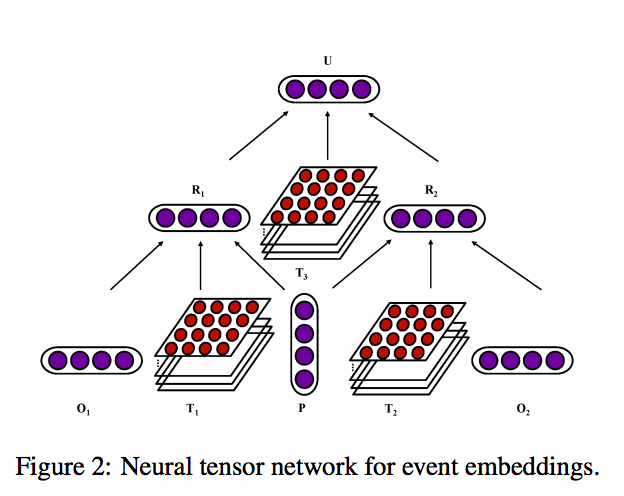

Each event has the form \(E = (O_1, P, O_2)\), where \(P\) is the action, \(O_1\) is the actor and \(O_2\) is the object on which the action is performed. For example, in the event “Google Acquires Smart Thermostat Maker Nest For for $3.2 billion.”, Actor is Google, Action is acquires and the Object is Nest.

Event Embeddings

They convert the news events into event embeddings. They do this using a 2-step process: first converting \(O_1\) and \(P\) to \(R_1\) and \(O_2\) and \(P\) to \(R_2\). \(R_1\) is computed by:

\[R_1 = f(O_1^TT_1^{[1:k]}P + W\begin{bmatrix} O_1 \\ P \\ \end{bmatrix} + b)\]In the second step, \(R_1\) and \(R_2\) are combined into the event embedding vector.

Model Description

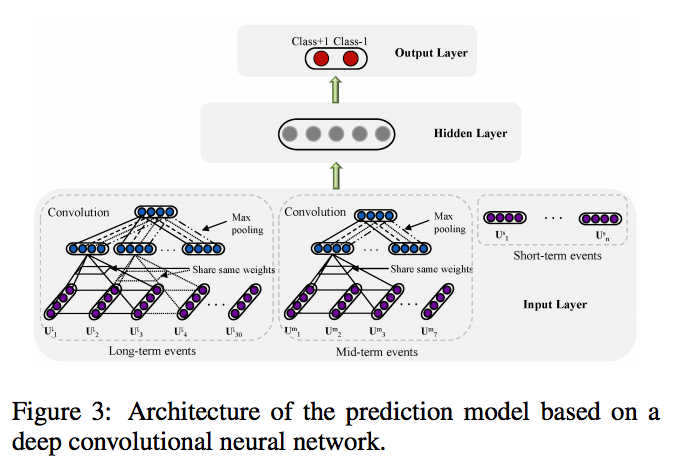

The news events are grouped into 3 categories:

- long-term events: Events over the past month

- mid-term events: Events over the past week

- short-term events: Events on the past day of the stock price change

In each case, they combine the events within each day by averaging the event embedding vectors. For long-term and mid-term sequences, they apply a convolutional layer of width 3 to extract localized features. Max pooling is applied to get the final dominant feature from each of them. Ultimately, they end up with feature vectors \(V^C = (V^l, V^m, V^s)\).

This feature vector is fed into a feed-forward neural network with one hidden layer and one output layer. This can be represented as: \(y_{cls} = f(net_{cls}) = \sigma(W_3^T \cdot Y)\) and \(Y = \sigma(W_2^T \cdot V^C)\).

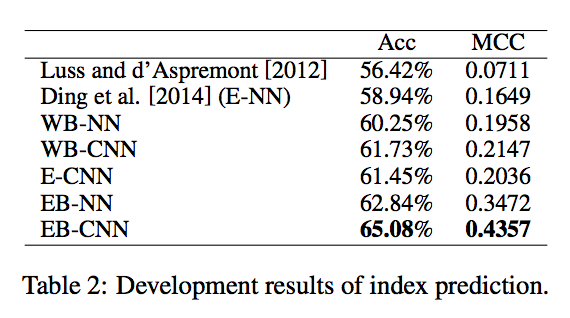

Results

- WB-NN: word embeddings input and standard neural network prediction model

- WB-CNN: word embeddings input and convolutional neural network prediction model

- E-CNN: structured events tuple input and convolutional neural network prediction model

- EB-NN: event embeddings input and standard neural network prediction model

- EB-CNN: event embeddings input and convolutional neural network prediction model

Comments

The event embedding aspect of the paper seems promising. It looks like a nice structured way to represent the events that can be used as an input to more concrete machine learning problems in finance.

While the authors have not released any code, there is a github repo available online that takes inspiration from this paper - even though the main idea of event embedding is missing in the linked code.